The Federal Motor Carrier Safety Administration will propose a rule Thursday that will, if made final, set criteria by which the agency could immediately revoke the operating authority of brokers and freight forwarders whose surety bonds or trust funds fall below the federally required $75,000 minimum. The agency is also seeking public input on a bevy of other issues as it relates to brokers who can’t pay carriers for loads tendered.

An advance notice of proposed rulemaking is scheduled for publication Thursday by FMCSA, and the agency will accept public feedback on the rule for 60 days — until November 27. The proposed rule implements statutes set by Congress in the six-year-old MAP-21 highway funding law, which required the agency to take steps in bolstering the solvency of brokers and freight forwards and to weed out those who aren’t. It also seeks feedback on a enforcement of these regs and definitions within the rule.

FMCSA will begin accepting comments on the proposed rule on Thursday at the regulations.gov portal via the Docket No. FMCSA-2016-0102.

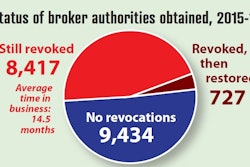

MAP-21’s most prominent change in broker regulation — boosting the minimum amount of surety bonds or trust funds required of brokers from $10,000 to $75,000 — was enacted by FMCSA in 2013. Thursday’s proposed rule is intended to ensure brokers meet that requirement and sets criteria for which the agency can revoke the operating authority of those who don’t.

Congress in MAP-21 stipulated that FMCSA should “immediately suspend” brokers or freight forwards who fall below the $75,000 requirement. That bond/credit requirement is there for carriers (like owner-operators) to file claims against for loads tendered if the broker does not pay them.

The agency proposes two broad situations for when it will suspend brokers’ authority to operate. 1) If it is notified by providers of bonds or trust funds that a brokers’ bond/fund has dipped below $75,000. 2) When a broker does not respond to a bond/fund provider when a claim is filed and the provider “determines the claim is valid and provides notice of these events to FMCSA.”

FMCSA says it is seeking feedback from industry stakeholders on “the appropriate cushion time” for brokers to respond to claims made against their surety bond or trust fund and about the due process concerns of shutting down a broker “without affording the company a chance to respond.” The agency intends to implement a process available for brokers whose authority is subject to being revoked.

The agency is also seeking public comments until Nov. 27 on adopting Congress’ statute that brokers’ and freight forwards’ trust funds consist of “assets readily available to play claims.” The agency says it first needs to define what “assets readily available” should consist of. It’s considering limiting it to cash and “FMCSA-approved letters of credit,” such as government bonds and notes, certified or cashier’s checks, irrevocable letters of credit “or other options that are easily convertible into cash,” FMCSA says.

The agency also seeks to define “financial failure” and “insolvency” as it relates to brokers and FMCSA’s ability to take action against insolvent brokers. MAP-21 requires surety bond providers to publicly advertise for 60 days when brokers fail financially so that carriers can make claims against these brokers’ bond/fund. However, FMCSA hopes to define the two terms above to make clear when bond providers must advertise. It’s also hoping to better codify what “publicly advertise” means.

FMCSA is also looking for input on whether “group surety bonds” are applicable to trucking and how the agency could regulate these types of set ups. It’s also seeking input on defining what a group surety bond is. However, the agency says it likely will not take action to allow group surety bonds, given their seeming complexity and the agency’s limited resources in regulating them.

Additionally, FMCSA is seeking feedback on whether BMC-85 trust providers, a current option for brokers to meet the $75,000 minimum requirement in contrast to BMC-84 surety bond providers, should be licensed and how it can ensure BMC-85 providers can pay claims brought by carriers.